For years, sodium-ion was talked about purely based on its potential: if the technology matures to where it’s competitive with lithium-ion, what would that mean for the battery industry?

Today, that discussion has taken a much different tone. With partnership announcements among industry titans, coverage from Wall Street analysts, and new products launching in the market, the conversation around sodium-ion has shifted so much you would think we were talking about the early growth spurt of lithium-ion.

Last month, Morgan Stanley Research published a 50-page note declaring the start of what it calls a “New Oil Age” for the energy industry because of sodium-ion batteries. The day after the note was released, the Financial Times published an article highlighting some of the major claims made by MS, including:

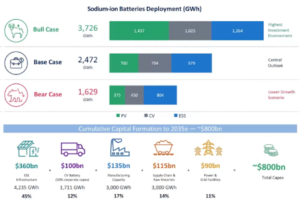

- “We predict sodium-ion batteries will take ~2 per cent market share by deployment in 2027, jumping to 20 per cent by 2030 and 37 per cent in 2035.”

- “Rather than a niche chemistry experiment, [sodium-ion] is becoming an $800bn capital formation wave by 2035, as the technology scales from pilot to industrial deployment”

- “The novel chemistry eliminates dependence on critical minerals such as lithium, copper, and graphite, so there’s a potential cost advantage of between 30 and 40 per cent over lithium iron phosphate (LFP) batteries.”

- “Sodium-ion ‘could unlock ~50% more energy storage demand by enabling greater attachment of ESS to renewables while allowing projects to reach economic parity with LFP.’”

The technical case for sodium-ion did not change overnight; cells have been shipping, cycling, and passing safety tests for some time. What changed is this: 1) the industry finally looked at the larger performance dynamics beyond simple cell-level energy density, and 2) there are now global companies putting big investment and production numbers behind sodium-ion. Those two shifts combined are pointing towards one thing: the sodium-ion era has arrived.

What the research says

Morgan Stanley’s research note is not incremental. The bank projects sodium-ion will hit 37% market share by 2035. It frames the buildout as an $800 billion capital formation wave over the next decade, a telltale sign sodium-ion is not a niche experiment but a full-stack infrastructure cycle touching utilities, grid operators, storage integrators, logistics, and equipment makers.

(source: Morgan Stanley Research via Financial Times)

PV = Passenger Vehicles; CV = Commercial Vehicles; ESS = Energy Storage Systems

The largest slice of that investment formation, $360 billion or 45% of the total, flows into energy storage system (ESS) infrastructure.

The basis for Morgan Stanley’s bullishness on sodium-ion for ESS is an expected 30–40% cost advantage over lithium iron phosphate (LFP) at the cell level, driven by a culmination of forces:

- Swapping expensive copper foil for cheaper aluminum in the current collector

- Independence from volatile lithium, cobalt, and graphite supply chains

- Rapidly declining production cost curves for sodium-ion cathodes, anodes, electrolytes, and current collectors

- Lower manufacturing overhead, as sodium-ion lines are largely compatible with existing LFP equipment and can ride the same learning curve.

Notably, MS’s ~36% cost-reduction estimate excludes future energy density gains, which would lower cost per kWh further.

What a 30%-40% Cost Evolution Means

Morgan Stanley’s logic is that these lower cell costs bring down the levelized cost of electricity (LCOE), making energy storage pencil out on projects that don’t clear the bar today. As that threshold falls, more projects move into economically viable territory — expanding the addressable market and potentially pushing global storage deployment well beyond current forecasts.

Because sodium-ion cells cost 30–40% less, a project can attach far more storage before it reaches cost parity with an equivalent LFP system — pushing the storage-to-solar PV attachment ratio much higher, to roughly 2.0x versus 1.4x for LFP in the US. At equivalent project economics, that means materially more storage per megawatt of solar, which MS estimates could raise effective demand for stationary storage in GWh terms by ~50% in its base case.

Sodium-ion’s cold-weather performance compounds the opportunity: retaining roughly 90% of capacity at –20°C (versus around half for LFP), it makes storage viable in northern geographies where AI infrastructure is scaling fastest — regions where LFP degradation and heavy thermal-management costs have held deployment back thus far.

The proofpoints are commitments now, not projections

Morgan Stanley puts forth a strong hypothesis, but the drumbeat of industry news on capital injections, product roadmaps, and signed supply agreements adds teeth to the projections the bank makes. Whether the hypothesis materializes rests on what the industry — from global majors to U.S. innovators — is actually doing:

CATL. CATL’s chairman is already on record saying he believes sodium-ion will take up to half of LFP’s market share, and the company’s 2026 activity tracks that view. In April, CATL signed a three-year, 60 GWh supply agreement with HyperStrong, one of China’s largest ESS integrators. In June, it announced both a 3.07 MWh sodium-ion 20-foot container at SNEC 2026 and TENER Sodium, a fully modular grid-scale system rated at more than 30 MWh per unit, with first deliveries scheduled for September. The world’s largest battery maker has moved sodium-ion from roadmap to signed contracts and shipping products.

BYD. BYD launched its grid-scale MC Cube-SIB sodium-ion storage product in 2024 using its proprietary blade battery form factor, and in early 2026 disclosed a third-generation cell rated for up to 10,000 charge-discharge cycles. Separately, BYD is investing roughly Rmb10 billion ($1.42B) into a 30 GWh plant aimed at ultra-affordable city cars. This is a major OEM treating sodium-ion as a portfolio strategy across both storage and vehicles.

GM and Peak Energy. General Motors has made its position public, with Kurt Kelty, GM’s VP of Battery and Sustainability, emphasizing there is “a right battery for the right application,” and for stationary energy storage, that battery is sodium-ion. The company is backing that statement with an exclusive partnership with Peak Energy and a strategic investment from GM Ventures that will result in GM developing sodium-ion cells in its Michigan battery labs with commercialization targeted for 2028. A U.S. automaker with in-house cell development capability has publicly named sodium-ion as its chemistry for grid storage and put capital behind it.

Alsym Energy. In April 2026, ESS Tech (NYSE: GWH) — a long-duration iron-flow storage maker — entered a strategic partnership to add 8.5 GWh of Alsym’s non-flammable Na-Series cells and modules to its portfolio. In May, California developer Juniper Energy committed to deploying 500 MWh of Alsym’s Na-Series storage across the state — including the Mojave Desert, where running without active cooling and qualifying for domestic-content tax credits is a direct economic edge. And in July, Alsym and ERITY signed a 9 GWh strategic relationship agreement to deploy non-flammable sodium-ion storage across mining operations, mobile AI data centers, and utility-scale projects in Australia, Africa, the Middle East, and beyond. With a cumulative 18 GWh in publicly announced customer commitments, Alsym represents the largest base of sodium-ion customer commitments outside of China.

The burden of proof has flipped

If you look at the announcements, a consistent message emerges: the benefits of sodium-ion are quickly establishing a new benchmark for stationary energy storage technology. The reasons cited across the industry are the same ones driving the Morgan Stanley thesis: a vastly more stable, non-FEOC supply chain; an all-around better safety profile; minimal cooling requirements slashing lifetime OpEx costs; a system life nearing 30 years; and faster charge and discharge without accelerated degradation.

The Morgan Stanley note and growing list of industry headlines mark a meaningful shift that the burden of proof has changed hands. Sodium-ion is now the chemistry that incumbents have to respond to, particularly lithium-ion as it continues to show inherent limitations around safety, supply chain, and performance.

In the face of a rapidly changing and growing storage market, the conversation has moved from whether sodium-ion belongs in the energy storage stack to how fast it scales and who builds it.

Learn more how Alsym Energy and its Na-Series are helping to answer those questions.